Money Advice Ontpeconomy: A Practical Guide to Building Financial Stability

Managing money wisely is one of the most important life skills anyone can develop. Financial stability does not happen by chance; it requires planning, discipline, and informed decision-making. In today’s fast-paced world where expenses are rising and economic conditions change frequently, understanding how to manage income, savings, and investments has become more important than ever.

Many people struggle with budgeting, saving for emergencies, or planning for long-term goals such as buying a home, starting a business, or preparing for retirement. Without proper financial guidance, it is easy to fall into debt or miss opportunities to grow wealth. This is why reliable guidance like money advice ontpeconomy can play an important role in helping individuals make smarter financial choices.

Financial education empowers people to control their money instead of letting money problems control their lives. Whether someone is just beginning their career or planning for retirement, the right financial strategies can make a significant difference. By understanding key financial principles, anyone can build a more secure future.

This article explores practical money management strategies, budgeting methods, saving techniques, investment ideas, and long-term financial planning. The goal is to help readers gain confidence in handling their finances and making informed decisions that support their goals.

Understanding the Importance of Financial Planning

Financial planning is the process of organizing your income, expenses, savings, and investments to achieve specific life goals. It helps people understand where their money goes and how they can use it more effectively.

Without financial planning, it becomes difficult to track spending or prepare for unexpected situations. Many individuals only think about money when problems arise, but proactive planning can prevent many financial challenges before they happen.

Following structured guidance such as money advice ontpeconomy can help individuals build a roadmap for financial success. This includes creating budgets, managing debt, and identifying opportunities to grow savings.

Financial planning also helps individuals prepare for major life events. These may include marriage, buying a home, education expenses, or retirement. Planning ahead allows people to allocate resources effectively and avoid unnecessary stress.

Another key benefit of financial planning is that it provides a sense of security. Knowing that you have a plan for emergencies and future goals creates peace of mind and allows you to focus on other aspects of life.

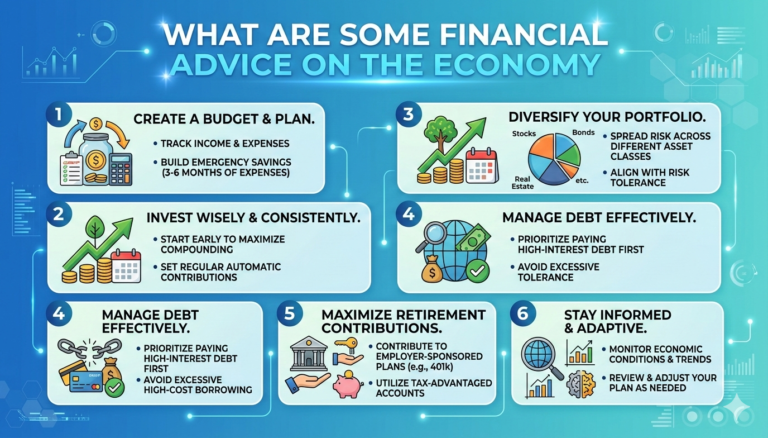

Creating a Realistic Budget

A budget is one of the most powerful tools for managing personal finances. It simply tracks how much money you earn and how much you spend. While budgeting may seem restrictive to some people, it actually provides freedom by giving control over financial decisions.

The first step in budgeting is calculating your total monthly income. This includes salary, business income, freelance earnings, or any other consistent source of money.

Next, list all monthly expenses. These typically fall into two categories: fixed expenses and variable expenses. Fixed expenses include rent, loan payments, and insurance, while variable expenses include groceries, transportation, and entertainment.

Many financial experts recommend the 50-30-20 budgeting rule. According to this method:

- 50 percent of income goes toward necessities

- 30 percent is used for personal spending

- 20 percent is saved or invested

By applying principles like money advice ontpeconomy, individuals can adjust their spending habits to match their financial goals. Small changes, such as reducing unnecessary purchases, can make a big difference over time.

A budget should not remain static. It must be reviewed regularly to ensure that it still reflects current income and expenses.

Building an Emergency Fund

Unexpected expenses are a normal part of life. Medical bills, car repairs, or job loss can create financial stress if there is no backup plan. An emergency fund acts as a financial safety net during such situations.

Most financial planners recommend saving at least three to six months’ worth of living expenses in an emergency fund. While this may seem difficult at first, it can be achieved gradually by setting aside a small portion of income each month.

One useful strategy is to automate savings. By automatically transferring money to a separate savings account, individuals can build their emergency fund without constantly thinking about it.

Financial frameworks like money advice ontpeconomy emphasize the importance of prioritizing emergency savings before making large investments. This ensures that unexpected events do not disrupt long-term financial plans.

Another important tip is to keep emergency funds easily accessible but separate from daily spending accounts. This reduces the temptation to use the money for non-emergency purposes.

Managing and Reducing Debt

Debt can be a major obstacle to financial stability if not managed properly. While some forms of debt, such as education loans or home mortgages, can be beneficial in the long term, excessive high-interest debt can quickly become overwhelming. ontpeconomy financial tips from ontpress

The first step in managing debt is understanding exactly how much you owe. Make a list of all debts, including credit cards, personal loans, and installment payments.

Two popular methods for paying off debt include:

The Snowball Method

This approach focuses on paying off the smallest debts first. Once the smallest debt is cleared, the payment amount is applied to the next debt.

The Avalanche Method

This strategy focuses on paying off debts with the highest interest rates first. This reduces the total interest paid over time.

Guidance like money advice ontpeconomy encourages individuals to choose the strategy that best matches their motivation and financial situation.

Avoiding new debt is equally important. Practicing mindful spending and using credit responsibly can prevent financial problems in the future.

Smart Saving Habits

Saving money is the foundation of financial security. Even small savings can grow significantly over time due to the power of compound interest.

One effective saving strategy is to treat savings like a fixed expense. Instead of saving whatever money remains at the end of the month, allocate a specific portion of income for savings at the beginning.

Another useful habit is setting clear financial goals. These goals might include:

- Buying a home

- Starting a business

- Funding education

- Traveling

- Retirement planning

When people save with a specific goal in mind, they are more likely to remain disciplined.

Financial resources such as money advice ontpeconomy highlight the importance of consistency when saving money. Regular deposits, even if small, can lead to meaningful financial progress.

It is also helpful to track savings growth periodically. Seeing progress can motivate individuals to continue their financial habits.

Understanding Investments

While saving money is important, investing allows individuals to grow wealth over time. Investments involve placing money into assets that have the potential to increase in value.

Common types of investments include stocks, bonds, mutual funds, and real estate. Each investment option carries different levels of risk and potential returns.

For beginners, diversification is a key principle. This means spreading investments across different asset types to reduce risk.

Education is essential before making investment decisions. Resources such as money advice ontpeconomy encourage individuals to understand market trends, risk tolerance, and long-term strategies before investing.

Another important concept is long-term investing. Short-term market fluctuations are normal, but long-term investments often benefit from steady growth.

Investors should also avoid emotional decisions. Panic selling during market downturns can lead to unnecessary losses.

Financial Education and Awareness

Financial literacy is a powerful tool that helps people make informed money decisions. Unfortunately, many individuals receive little financial education during their early years.

Learning about budgeting, saving, investing, and debt management can significantly improve financial outcomes.

Educational resources, workshops, and financial guides play an important role in increasing financial awareness. Following structured knowledge systems such as money advice ontpeconomy can provide practical insights into managing personal finances.

Reading financial books, listening to podcasts, and attending seminars are also effective ways to expand financial knowledge.

The more individuals understand about money management, the more confident they become in making financial decisions.

Global Perspectives on Personal Finance

Money management principles apply worldwide, but financial environments differ between countries. Economic policies, taxation systems, and investment opportunities vary across regions.

For example, financial planning strategies used in the United States may differ from those in other parts of the world due to different economic structures and retirement systems.

Despite these differences, the core principles of financial success remain consistent. Budgeting, saving, and investing responsibly are universal practices.

Frameworks like money advice ontpeconomy emphasize adaptable strategies that individuals can apply regardless of their location or income level.

Understanding global financial trends can also help individuals make better investment decisions and recognize economic opportunities.

Developing Long-Term Financial Goals

Long-term financial planning helps individuals stay focused on their future objectives. These goals may include financial independence, retirement planning, or building generational wealth.

The first step is identifying clear goals. For example, someone may want to retire comfortably by a certain age or accumulate a specific amount of savings.

Once goals are defined, it becomes easier to create a strategy for achieving them. This may involve consistent investing, increasing income streams, or reducing unnecessary expenses.

Approaches like money advice ontpeconomy highlight the importance of reviewing financial goals regularly. Life circumstances change, and financial plans should adapt accordingly.

Another helpful strategy is breaking large goals into smaller milestones. Achieving smaller targets builds confidence and keeps individuals motivated.

The Role of Discipline and Mindset

Financial success is not determined solely by income level. Mindset and discipline play equally important roles.

Many people with high incomes still struggle financially because they lack spending control. On the other hand, individuals with modest incomes can achieve financial stability through careful planning and discipline.

Developing healthy financial habits requires patience and consistency. Avoiding impulsive purchases, tracking expenses, and sticking to a budget are all important steps.

Resources like money advice ontpeconomy emphasize that long-term financial success is built through daily habits rather than sudden changes.

A positive financial mindset also encourages individuals to view money as a tool for achieving goals rather than a source of stress.

Conclusion

Financial stability is achievable for anyone willing to learn and apply sound money management principles. Budgeting, saving, investing, and managing debt are essential components of a strong financial foundation.

While financial challenges may arise, having a clear plan makes it easier to overcome obstacles and stay focused on long-term goals. By developing financial discipline and increasing financial knowledge, individuals can improve their economic well-being.

Guidance such as money advice ontpeconomy highlights the importance of practical strategies that help people make better financial decisions. These strategies encourage individuals to take control of their money, build emergency savings, reduce debt, and invest wisely.

Ultimately, financial success is not about quick gains or shortcuts. It is about consistent effort, thoughtful planning, and a commitment to building a secure future. By following proven financial principles, anyone can move toward greater financial freedom and stability.